Every property manager has the same Friday afternoon ritual. Open the compliance spreadsheet. Filter for "missing." Send the reminder emails. Mark off the certificates that came in. Move the ones that didn't to next week.

It's one of the most thankless workflows in property management, and one of the most operationally expensive. PMs spend hours per week chasing renter's insurance proof from residents, reviewing third-party certificates from carriers they've never heard of, and hoping the policies they collected at lease signing are still in force six months later.

They usually aren't. And no one tells you when they lapse.

The hidden problem: silent lapses

Most renter's insurance policies don't get cancelled on purpose. They lapse… the resident's auto-pay fails, they switch carriers without telling the landlord, or they discontinue the policy after a few months when nothing has gone wrong. The certificate in the PM's file shows valid coverage. The actual policy is gone.

This is the gap that hurts. A claim happens. The PM pulls the file. The certificate looks fine. The carrier confirms the policy lapsed three months ago.

By then, the owner is exposed, the resident has no coverage for their belongings, and the property manager is fielding three difficult phone calls at once.

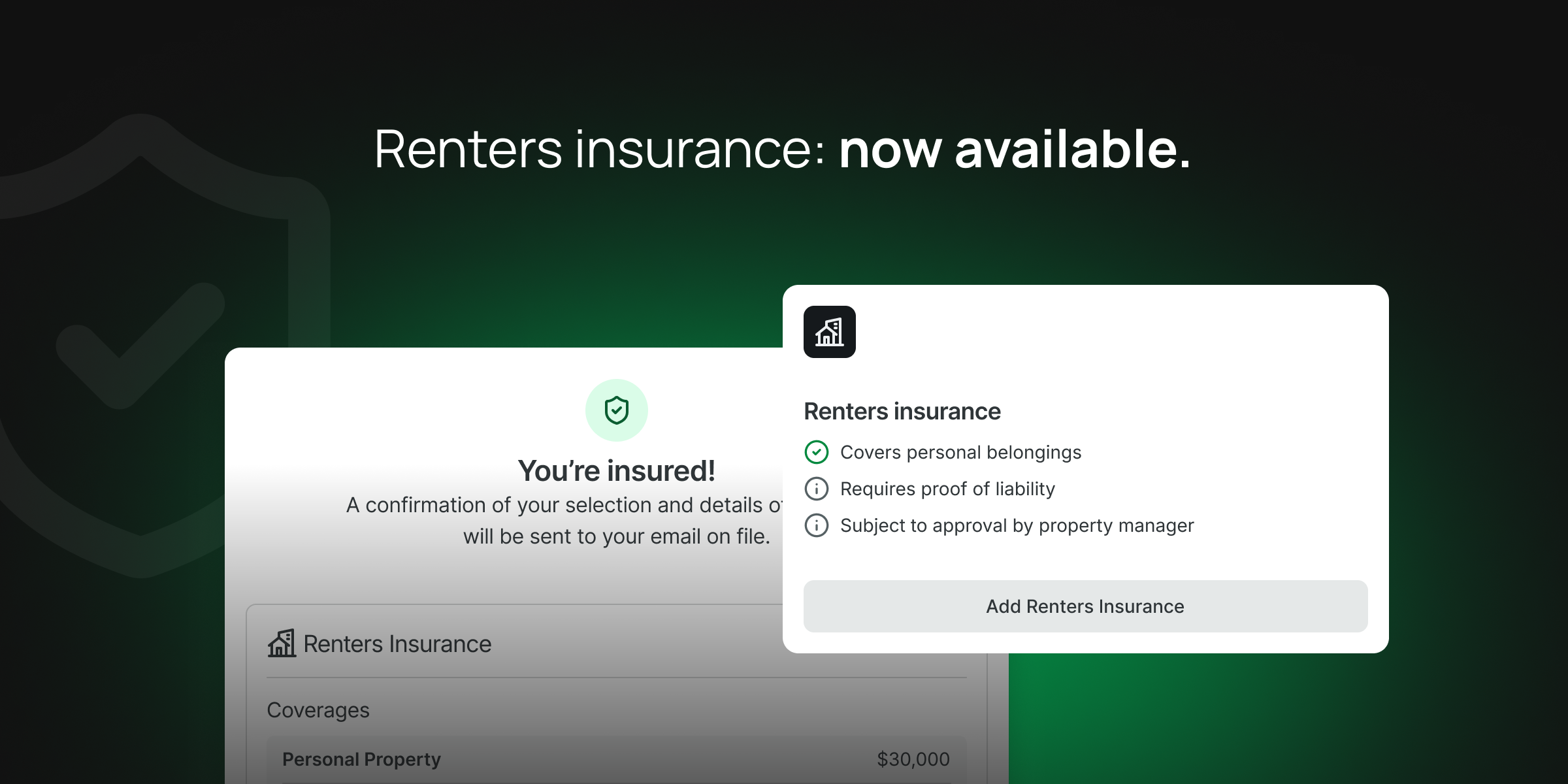

What HO4 actually is

HO4 is the formal name for renter's insurance: the standard ISO policy form designed to cover a tenant's personal property and liability. It's the policy property managers reference when their lease requires "proof of renters insurance."

A typical HO4 policy includes:

Personal property coverage: the resident's belongings (furniture, electronics, clothing) up to a stated limit, often $100,000 in modern policies

Liability coverage: protects the resident if they cause damage or injury, with limits typically $100K or $300K

Loss of use: temporary living expenses if the unit becomes uninhabitable

Medical payments: small medical claims for guests injured at the home, regardless of fault

Add-ons: replacement cost endorsements, pet bite coverage, roommate coverage, animal liability limitations

HO4 doesn't cover the building itself. That's the landlord's responsibility through a DP3 or owner’s policy. HO4 covers the resident's stuff and the resident's liability exposure.

Where the PM workflow breaks

The problem isn't HO4 itself; it's how property managers interact with it. The typical workflow has three failure points:

Verification at signing. Residents present a certificate from an outside carrier. The PM has to verify the policy is actually in force, covers the required limits, and lists the property correctly. Often the certificate arrives day-of, holding up move-in.

Tracking over time. Once filed, the certificate sits. There's no automated way to know if the policy stays active. PMs default to spreadsheets, reminders, and good intentions.

Lapse detection. When a policy cancels, the carrier notifies the policyholder, not the property manager. The PM finds out only if the resident tells them (rare) or after a claim (too late).

Every one of these failure points costs the team time, and the third one costs owners money.

How HO4 inside the workflow changes the equation

Renter's insurance that's enrolled inside the property management workflow flips all three failure points:

Verification disappears. When residents enroll during the leasing flow, the policy is issued instantly with the property correctly listed and the required limits already met. No verification needed. No certificate to chase.

Tracking is automatic. Policy status lives on the lease record. There's no spreadsheet to maintain because the data is already where the PM is working.

Lapses get reported. The Tenant Additional Interest Endorsement, a standard policy add-on, automatically notifies the property manager when a policy is cancelled. The PM finds out the same day. Not after a claim.

That last piece is the one that matters most. Lapse visibility is the difference between renter's insurance as a compliance theater exercise and renter's insurance as actual risk management.

Where HO4 fits in the broader insurance stack

HO4 isn't the only policy in play. A complete insurance picture for a residential rental includes:

TLL (Tenant Legal Liability): protects the owner's structure from accidental tenant-caused damage, owned by the property management company

HO4 (Renter's Insurance): protects the resident's belongings and liability, owned by the resident

DP3 (Landlord Insurance): protects the owner's structure, owned by the owner

The three policies don't overlap. They cover different parties for different exposures. HO4 plus TLL together close the gap most property managers worry about: when a resident lets their coverage lapse, TLL backs up the owner. When HO4 is in force, it does what it was designed to do.

The bottom line

Renter's insurance compliance isn't a problem you solve once at lease signing. It's a problem you solve continuously, for the life of the lease. Built-in HO4 with lapse alerts, standardized coverage, and compliance status inside the property management software, turns a recurring operational drain into background infrastructure.

The certificate chase doesn't need a better filing system. It needs to go away.

To learn how Rentvine HO4 and TLL work together, learn more here: https://www.rentvine.com/rentvine-insurance